India's Smartphone Market Continues to Grow in 2025

Smartphone Shipments in India on the Rise

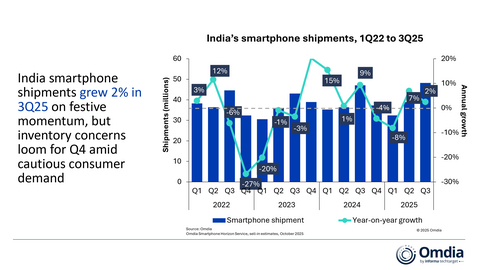

Omdia's latest research indicates that India's smartphone market is set to grow by %3 to reach 48.4 million unit shipments in the third quarter of 2025. With high demand expectations for the festival season, suppliers have filled their channels with new stock. New launches in July and August, retail incentives, and an earlier festival season have driven modest growth.

vivo (excluding iQOO) maintained its market leadership with 9.7 million units shipped, capturing a %20 market share. Samsung ranked second with 6.8 million units and a %14 market share. Xiaomi, holding a %13 market share, ranks third, shipping 6.5 million units alongside OPPO. Apple re-entered the top five with 4.9 million units, making progress thanks to growth from smaller cities.

Sanyam Chaurasia, Omdia Lead Analyst, stated, "With limited organic demand, third-quarter momentum was largely driven by incentive-led channel pushes." Suppliers have reallocated marketing budgets impacting the entire product range with cash bonuses per unit that reward sales. These incentives motivated distributors and retailers to absorb high stocks ahead of the festival period. At the same time, consumer-focused plans increased; zero down payment installment options, micro-installment plans, and extended warranties were offered to boost conversions.

vivo strengthened its market leadership with a balanced portfolio, aggressive retail programs, and a prominent promotional network. The T series scaled rapidly online during the festival period. Samsung gained strength in the mid-segment market with refreshed models like the S24 and S25 FE, but faced pressure in the entry level. OPPO experienced significant volume growth with a multi-layered festival program centered around the F31 series. Outside the top five, Motorola broke records with 4 million units and showed %53 growth through the offline expansion of the G series and Edge 60. The brand Nothing grew by %66, invigorating the market with the CMF Phone 2 Pro and Phone 3a.

Apple achieved its highest shipments in India during Q3, capturing a %10 market share. Demand from smaller cities, bold festival campaigns, and a wider product range spurred this growth. Discounts on older iPhone 16 and 15 models facilitated significant shipments, while the iPhone 17 base model received support from the existing user base.

The gains in the third quarter are unlikely to continue strongly as the year progresses. While government-backed reforms have boosted overall retail optimism, the increase in smartphone demand remains limited. Urban consumers continue to postpone upgrades due to uncertainty in job security and rising cost sensitivity. This scenario raises concerns about inventory buildup in Q4.

```Sizin İçin Derlendi

Benzer Haberler

.png)

Yakında Tüm Platformlarda

Sizlere kesintisiz haber ve analizi en hızlı şekilde ulaştırmak için. Yakında tüm platformlarda...

.png)