Google Balance Sheet: The Effects of Artificial Intelligence and the Cloud

Google Earnings Report: Key Concerns

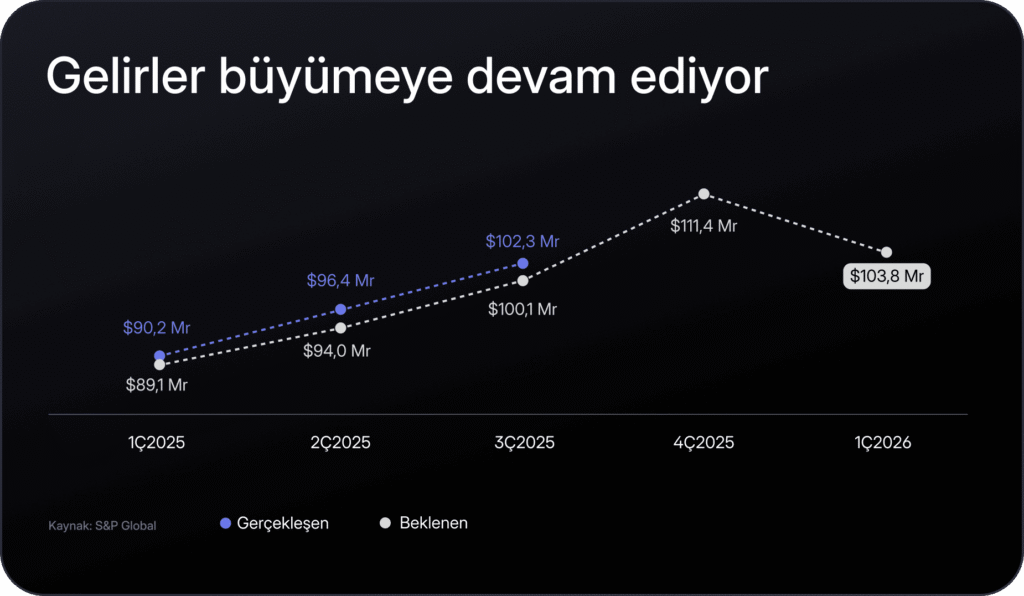

Google will release its earnings report after market close on Wednesday, February 4th. This report presents an important opportunity to test the return on investment from the company’s artificial intelligence expenditures.

Revenue Expectations and Growth Focus

According to consensus expectations, Google’s quarterly revenue is expected to be $111.4 billion. This figure represents an over 15% growth compared to the same period last year, potentially demonstrating the company's momentum in artificial intelligence.

Particularly, the expected 35% growth of Google Cloud is drawing attention. However, how increasing infrastructure costs will affect this growth remains a significant question mark.

Waymo and AI Investments

Waymo, under Alphabet, raised its valuation to $126 billion with $16 billion in funding. Increased competition and safety scrutiny in the autonomous driving sector create uncertainties regarding the project's sustainability.

Additionally, the details of the Siri-Gemini integration agreement with Apple enhance Google’s potential for new revenue streams. These developments provide vital clues about how Google can maintain its dominance in the search engine market.

Risk Factors and Market Reactions

Rising competition and regulatory pressures pose risk factors for Google’s stock values. In particular, lawsuits initiated by the U.S. Department of Justice threaten long-term valuations.

Currently, options markets are pricing in a volatility of about 5% following the earnings report. Investors are closely monitoring how much profit this quarter’s revenue generates and how revenue growth reflects on margins.

Post-Earnings Expectations

The high capital expenditures for Google’s AI infrastructure remain a significant topic of discussion. If expenses come in above expectations but fail to present a clear net income story, there may be pressure on the stock. Particularly, the expansion of operating margins in the cloud segment will demonstrate how well the company is benefiting from economies of scale.

Sizin İçin Derlendi

Benzer Haberler

.png)

Yakında Tüm Platformlarda

Sizlere kesintisiz haber ve analizi en hızlı şekilde ulaştırmak için. Yakında tüm platformlarda...

.png)